If you're running a crypto business in Europe-or even just holding digital assets-you can't afford to ignore the EU's new sanctions and compliance rules. As of December 30, 2024, the Markets in Crypto-Assets Regulation (MiCA) became fully active, and with it came a sweeping overhaul of how crypto is treated under EU law. This isn't just another set of guidelines. It's a legal framework with teeth. Miss a requirement, and you could face fines, a shutdown, or even a ban across all 27 EU countries.

What MiCA Actually Does

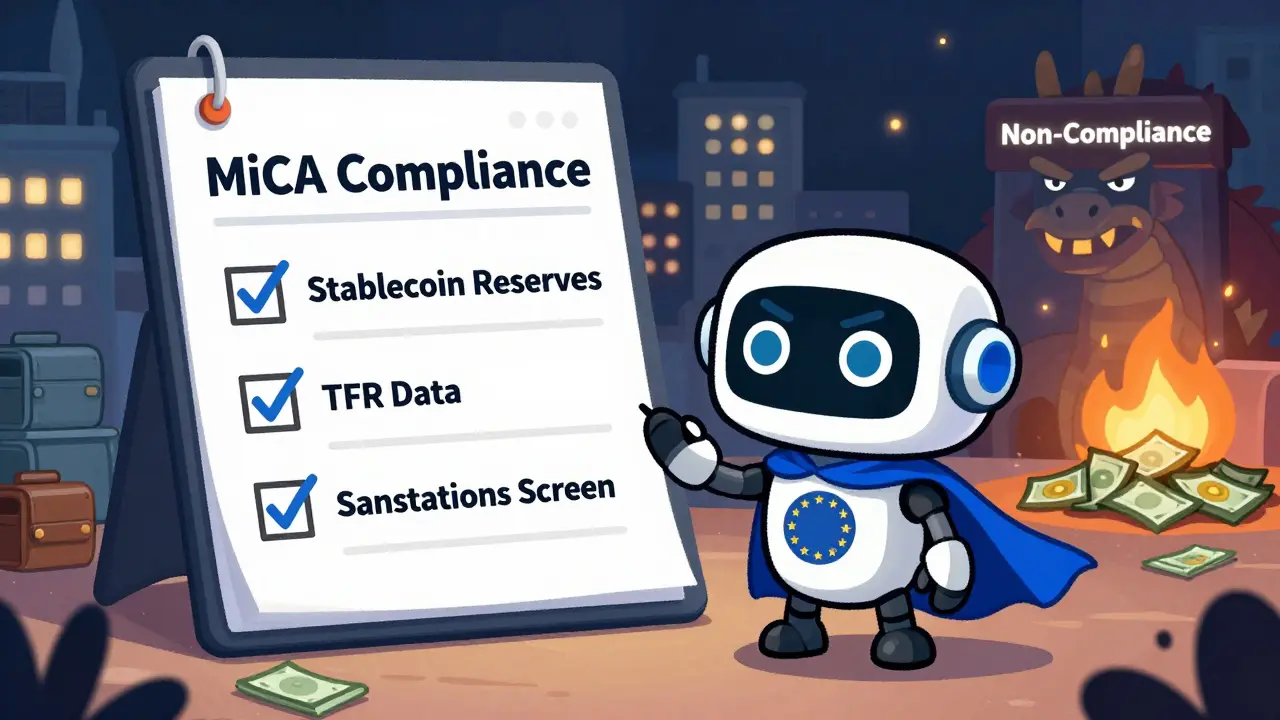

MiCA doesn't just regulate crypto. It brings crypto under the same kind of oversight as banks. Before MiCA, crypto firms operated in a patchwork of national rules. Now, if you're a Crypto Asset Service Provider (CASP)-that's any exchange, wallet, or trading platform serving EU users-you need official authorization. You can't just start operating. You must apply, prove you have proper systems, and get approved by your national regulator. The regulation covers everything from stablecoins to utility tokens. But the real focus is on stablecoins. If your token is meant to hold value by backing it with euros or other assets, you need to hold 1:1 reserves in liquid form. Daily transaction limits? Cap at €200 million. Launch a new stablecoin without approval? Illegal. The European Central Bank is watching closely, and they're not interested in crypto undermining the euro.The Transfer of Funds Regulation (TFR): No Grace Period

One of the most aggressive parts of the EU's crackdown is the Transfer of Funds Regulation (TFR). It went live on the same day as MiCA-December 30, 2024-and there was no grace period. Zero. No exceptions. No "we'll let you off this time." TFR requires every crypto transfer over €1,000 to carry full sender and recipient data. That means names, addresses, account numbers-even if the transaction goes from a wallet to another wallet. CASPs must collect this info at the point of origin and pass it along to the receiving platform. If the receiving platform doesn't comply, the transaction gets blocked. This is a massive technical lift. Most wallets and decentralized exchanges didn't have this built in. Now they're scrambling. Some platforms simply stopped serving EU users rather than rebuild their systems. Others invested millions in compliance software. The goal? To stop criminals from using crypto to launder money or evade sanctions.Sanctions Enforcement: It's Not Optional

The EU doesn't just want you to follow the rules-it wants you to actively stop sanctioned entities from using crypto. That means integrating real-time sanctions screening into your transaction monitoring systems. If someone on the EU's sanctions list tries to send or receive crypto through your platform, you must freeze the transaction and report it immediately. This isn't theoretical. In early 2025, a Lithuania-based crypto exchange was fined €4.2 million after it processed transfers linked to a Russian entity under EU sanctions. The regulator found they hadn't updated their screening tools in over six months. That's not negligence-it's a violation. You also need to monitor for suspicious activity. That includes unusual transaction patterns, rapid movement of funds between wallets, or repeated attempts to bypass address checks. If you see red flags, you file a Suspicious Transaction Report (STR) with your national financial intelligence unit. Failure to do so can result in criminal charges.

DORA and CARF: The Hidden Layers

MiCA and TFR are the headline rules, but they're not the only ones. Two other regulations are quietly tightening the screws. The Digital Operational Resilience Act (DORA) kicked in on January 17, 2025. It forces crypto firms to prove they can survive cyberattacks, system failures, or third-party outages. You need documented backup plans, regular penetration tests, and proof that your cloud providers meet EU security standards. If your platform goes down because you didn't test your recovery system? That's a compliance failure-and it can trigger sanctions. Then there's the Crypto-Asset Reporting Framework (CARF). By 2026, every CASP must report user tax data to local tax authorities. This includes transaction history, wallet addresses, and asset holdings. Think of it as the EU's version of FATCA, but for crypto. If you don't report, you risk fines, license revocation, or being added to a public non-compliance list.What Happens If You Don't Comply?

The consequences aren't just financial-they're existential. - Fines: Up to 5% of annual turnover or €5 million, whichever is higher. For a small exchange, that could mean shutting down. - License Revocation: Your authorization to operate in the EU is pulled. No more serving EU customers. - Blacklisting: Your company name gets added to a public EU sanctions list. Banks will refuse to work with you. Payment processors will cut you off. - Criminal Liability: In cases of deliberate evasion or laundering, executives can face personal liability. There's no "I didn't know" defense. Regulators expect you to stay current. They don't care if you're a startup with two employees. If you serve EU users, you're bound by EU law.How Do You Stay Compliant?

Here’s what actually works in 2026:- Get authorized under MiCA. Don't wait. The transitional period ended in mid-2025.

- Implement TFR-compliant transaction monitoring. Use a certified vendor-don't try to build it yourself.

- Integrate real-time sanctions screening. Use tools that pull from the EU's official sanctions list and update automatically.

- Train your team. Every customer support rep, developer, and compliance officer needs to know what a red flag looks like.

- Prepare for CARF. Start collecting tax data now. Don't wait until 2026 to realize you don't have it.

- Document everything. Regulators will ask for logs, training records, and audit trails. If you can't produce it, you're non-compliant.

Harshal Parmar

January 25, 2026 AT 06:16Man, I've been watching this EU crypto crackdown from India and honestly? It's kind of inspiring. I mean, sure it's strict, but at least they're trying to build something real instead of letting the wild west keep eating itself. We don't have the same infrastructure here, but seeing how they're forcing transparency makes me want to push harder with my own small crypto education project. No more shady ICOs, no more rug pulls disguised as 'decentralized finance'-just clear rules. It’s not perfect, but it’s a start. And honestly? I think other regions will follow. The EU doesn't play around, and that’s kind of beautiful in its own way.

Sara Delgado Rivero

January 25, 2026 AT 18:07So now we have to track every single wallet transfer like we're the FBI and everyone's a money launderer? This is just fascism dressed up as regulation. The EU thinks they can control blockchain by forcing KYC on every transaction? Bro they literally built a system to avoid this exact thing. Now they're turning crypto into a bank with worse UX. I'm not even mad I'm just impressed at how badly they're missing the point

Jessica Boling

January 27, 2026 AT 14:47Oh sweet jesus the EU just turned crypto into a DMV with a blockchain logo. You gotta submit a form, get approved, install software, train your entire team, and pray your cloud provider doesn't get hacked all before you can let someone send 1000 euros to their cousin. Meanwhile in the US we're just like hey cool NFTs can I get a pizza? The EU didn't tame crypto they just made it wear a suit and carry a clipboard everywhere. And don't even get me started on CARF. Now my crypto gains are gonna show up on my tax return like I'm filing for unemployment

Tammy Goodwin

January 28, 2026 AT 04:37I get that they want to stop criminals but this feels like using a sledgehammer to kill a fly. Most people using crypto aren't laundering money they're just trying to send money to family overseas without paying 10% in fees. And now you're forcing every small wallet to become a compliance officer? That's not protection that's punishment. And for what? So the ECB can push their digital euro? I'm not convinced this is about security anymore

Shamari Harrison

January 29, 2026 AT 03:15For anyone new to this-don't panic. MiCA isn't the end of crypto it's the beginning of legitimacy. If you're a legit business, compliance isn't a burden it's your competitive advantage. The platforms that follow these rules will be the ones people trust. The ones that don't? They'll vanish. Start with MiCA authorization, use a certified TFR vendor, and don't try to DIY your sanctions screening. It's expensive upfront but way cheaper than getting fined €5 million. And yes, CARF is coming. Start collecting wallet data now. Your accountant will thank you in 2026.

katie gibson

January 30, 2026 AT 16:16so like the EU just turned crypto into a 9 to 5 job with extra paperwork and no coffee breaks?? i mean i get it they dont want russian oligarchs buying solana with dirty cash but now i gotta prove i didnt buy my bitcoin from a guy named "vodka" in a reddit DM?? like why am i being punished because some guy in russia is bad at hiding money?? also why is everyone acting like this is new?? weve been saying this for years lol

Ashok Sharma

January 31, 2026 AT 06:59This is good for the industry. In India, many people are scared of crypto because they think it is illegal or unsafe. Now, with clear rules, people will understand that crypto is not a gamble. If you follow the law, you are safe. The EU is showing the world how to do it right. We should learn from this. Small businesses need support, not fear. Compliance is not a burden. It is a path to trust.

Margaret Roberts

February 1, 2026 AT 09:44Let me guess… this is all just a trap to get us to use the digital euro. They don't care about criminals they care about control. The moment you force every transaction to be tracked, you own the money. This isn't regulation it's surveillance. And don't tell me they won't abuse it. The same people who wrote this are the ones who told us 5G was harmless. Wake up. They're building a financial panopticon and they want you to sign the waiver with your wallet address

Jen Allanson

February 2, 2026 AT 18:20It is imperative that all entities operating within the jurisdiction of the European Union adhere strictly to the regulatory mandates established under MiCA, TFR, DORA, and CARF. Failure to comply constitutes a material breach of international financial governance norms and exposes both institutional and individual actors to severe civil and criminal penalties. The absence of a grace period is not an oversight-it is a deliberate assertion of sovereign regulatory authority. One must not mistake legal clarity for oppression.

Barbara Rousseau-Osborn

February 3, 2026 AT 02:42Ohhhhh so now you need a PhD in compliance just to send your buddy 500 euros in ETH?? 😂 You people are literally turning freedom into a form you have to file in triplicate. And the digital euro?? Please. That's just the government's way of saying "we're taking your money back." I'm moving my crypto to a non-EU wallet. And if you think they won't freeze your account for a "suspicious pattern" because you bought a coffee with BTC? You're delusional. #CryptoIsDead #DigitalEuroIsTheNewTaxes

george haris

February 3, 2026 AT 09:19Big thanks for breaking this down so clearly. I was totally overwhelmed by all the acronyms but now I get it. MiCA is like the foundation, TFR is the gatekeeper, CARF is the taxman knocking at your door. And DORA? That's just the fire drill you didn't know you needed. Honestly, if you're building something real in crypto, this is a gift. It's not about being scared-it's about being ready. And if you're just holding crypto? Start talking to your tax person. Don't wait till April 2026. You'll thank yourself later.

Melissa Contreras López

February 4, 2026 AT 23:39Okay but can we just appreciate how wild it is that the EU is the one actually trying to make crypto work for the people instead of just letting Wall Street loot it? I know it feels like a cage but honestly? It’s the cage that keeps the lions out. I’ve seen too many friends lose everything to shady platforms. Now? At least they can say "Hey, this exchange is MiCA-approved" and actually mean it. Yeah it’s a pain. But if we want crypto to be more than a casino, this is the price of admission.

Mike Stay

February 6, 2026 AT 05:32The European Union's regulatory architecture represents a paradigmatic shift in the governance of digital asset ecosystems. Unlike the fragmented, enforcement-driven model of the United States, the EU has pursued a harmonized, principle-based framework grounded in systemic stability and consumer protection. The confluence of MiCA, TFR, DORA, and CARF constitutes a comprehensive regulatory matrix that anticipates operational, financial, and cyber-resilient risks. This is not overreach-it is institutional maturity. The United States, by contrast, remains mired in regulatory arbitrage and political gridlock. The future of global finance is not decentralized chaos-it is regulated integrity.

Taylor Mills

February 8, 2026 AT 04:17USA still runs the world. EU thinks they can just slap rules on crypto and call it a day? Bro they dont even have the tech to make their own trains run on time. And now they want to control my wallet? I dont care if they ban me from their market. I'll just use US platforms. And if you think the digital euro is gonna save them? Good luck getting anyone to use it when you can just buy BTC with a credit card in 2 seconds. This is Europe trying to be the boss when they dont even own the game

Arielle Hernandez

February 9, 2026 AT 19:44It's worth noting that CARF's reporting obligations are aligned with OECD standards and will be interoperable with global tax authorities. This is not an EU-specific power grab-it's part of a coordinated international effort to close tax loopholes in decentralized finance. The fact that the U.S. has not yet adopted similar frameworks is a gap, not a virtue. Compliance isn't about surrendering freedom; it's about ensuring the integrity of the financial system. If you're holding crypto legitimately, you have nothing to fear from transparency.

HARSHA NAVALKAR

February 10, 2026 AT 18:00Why does everyone have to be so loud about it? I just want to hold my Bitcoin in peace. Why do I have to read all this? Why can't they just let me be? I don't even trade. I just bought some years ago and forgot about it. Now I'm scared to even open my wallet. Why do they have to ruin everything? I just wanted to be left alone...

Ryan Depew

February 12, 2026 AT 00:43So TFR means if my buddy sends me 1200 euros in ETH from his Coinbase wallet, I gotta give him my full name, address, and birth certificate? Bro that's not crypto that's banking with extra steps. And if he's using a non-compliant wallet? Transaction gets blocked? So now I gotta convince my friends to use the same platform? That's not freedom that's a loyalty program. And the worst part? I'm the one who gets blamed if I don't know his address. I don't even know where my cousin lives half the time

Mathew Finch

February 13, 2026 AT 20:06Let me get this straight-the EU wants to regulate crypto because it's a threat to the euro? So they're not worried about criminals they're worried about competition? The digital euro is their Plan B for when people realize central banks are just printing money. This isn't about safety. This is about control. And if you think the ECB is gonna let decentralized money exist without turning it into a tax-collecting robot? You're dreaming. Crypto was supposed to break chains. Now it's just another government app

Andy Simms

February 13, 2026 AT 23:28If you're a small dev or startup trying to build something in crypto and you're reading this-don't give up. The compliance burden is real, but there are tools out there. Use regulated KYC providers. Automate your sanctions screening. Don't try to build it from scratch. And yes, CARF is scary-but if you start collecting wallet addresses and transaction dates now, you'll be ahead of 90% of the market. This isn't the end of crypto. It's the end of the Wild West. And honestly? We needed it.

Tselane Sebatane

February 14, 2026 AT 06:40As someone from South Africa where banking is a nightmare and remittances cost 20%, seeing the EU do this makes me feel hopeful. Yes, it's strict. But imagine if every country had rules this clear? No more shell companies. No more hidden wallets. No more people losing life savings to fake exchanges. I know it's hard for small players but if we want crypto to be fair for everyone-not just the rich with lawyers-this is the way. I'm not saying it's perfect but it's the first time I've seen a major economy treat crypto like a real financial system instead of a gamble

Jonny Lindva

February 14, 2026 AT 20:26Honestly I'm kinda proud of the EU for doing this. I know it sounds harsh but if you're building something real in crypto, you want rules. It gives you credibility. I've seen too many projects get shut down because they didn't follow anything. Now? You can say "we're MiCA-compliant" and people actually trust you. Yeah it's a headache but it's the kind of headache that means you're not gonna get robbed tomorrow. Just take it step by step. You got this.

Matthew Kelly

February 16, 2026 AT 15:10Just wanna say I moved my whole portfolio to a non-EU wallet last week. Not because I'm hiding anything but because I don't wanna be forced to hand over my personal info every time I send 100 bucks. And now my favorite dApp won't let me connect? Bro I just wanted to play a game. Why does everything have to be a bank now? 😔

Linda Prehn

February 16, 2026 AT 19:57So the EU is basically saying if you want to use crypto you have to be a corporate entity with a compliance team? That's not innovation that's a joke. And CARF? So now my crypto is gonna be reported to the IRS and the EU at the same time? I'm gonna have to file two tax returns just to prove I didn't steal anything? I'm not a criminal I'm just someone who believes in decentralization. Why does the government always have to ruin the fun?

Adam Lewkovitz

February 16, 2026 AT 23:46USA is the real winner here. We don't have some bureaucrat telling us how to use our money. We let the market decide. The EU is just scared because their economy is falling apart and they think crypto will replace the euro. Newsflash: it won't. People want freedom not forms. If you're in the EU and you're mad about this? Move. Go to the US. We got pizza, freedom, and no one's asking for your birth certificate to send ETH

Clark Dilworth

February 17, 2026 AT 19:55From a systems architecture standpoint, the integration of TFR with MiCA's CASP authorization framework creates a non-repudiation layer that fundamentally alters the trust model of peer-to-peer value transfer. The mandatory metadata propagation enforces a centralized audit trail within a decentralized ledger paradigm-a technical paradox that necessitates novel cryptographic accountability primitives. The regulatory imperative is clear: decentralization cannot imply opacity. CARF's standardized data schema, aligned with ISO 20022, ensures interoperability across jurisdictional boundaries-a necessary precondition for global financial stability in the tokenized economy.

Brenda Platt

February 18, 2026 AT 15:57Y'all are making this way harder than it needs to be 😊. Yes, the rules are strict-but think of it like getting a driver's license. You gotta show ID, pass a test, follow traffic laws. That doesn't mean you can't drive. It means you can drive safely. If you're holding crypto for yourself? Just keep good records. If you're running a platform? Get help. There are so many great compliance tools out there now. You're not alone. And if you're scared? That's okay. Take a breath. Start small. One step at a time. You got this 💪✨

Melissa Contreras López

February 20, 2026 AT 05:50Reading all these comments makes me realize something-we're all just trying to figure out how to survive in a world that's changing faster than we can adapt. The EU didn't make crypto evil. They just made it real. And maybe that's the hardest part. Not the rules. But the fact that we have to grow up.

Shamari Harrison

February 21, 2026 AT 17:57Exactly. This isn't about killing innovation. It's about making sure innovation doesn't leave people behind. The first wave of crypto was about freedom. The next wave is about responsibility. And honestly? We need both.